ESG Reporting in 2025: Why Waiting Is the Riskiest Option

Uncertainty is not a strategy

If you’re running a business in the EU right now, “regulatory freeze” probably feels like the new normal. Since early 2025, ESG reporting rules have been reshuffled by the Omnibus proposal. Timelines shift, definitions evolve, and no one seems certain what will be required, or when. Yet the Commission’s fresh Recommendation on VSME sends a clear message: SMEs should prepare to report - sooner, not later. Do you keep investing in your ESG reporting solution, or pause and risk lagging behind?

Pausing is risky & would you? Banks already price loans with ESG data in mind, insurers load premiums based on climate exposure, and major buyers demand transparent supply-chain metrics. In other words, ESG data reporting has moved from “compliance box-tick” to “must-have business credential.” With VSME now formally recognised, those data expectations will converge on one standard.

This guide gathers insights from banks, investors, policy-makers, and SMEs to show how ESG reports are being used today - not just after the the EU has made up their mind - and why starting now is the smartest move you can make.

The Risks Are Real: Climate Is Impacting Businesses Today

Climate hazards in Europe are no longer future threats, they’re already cutting into profit margins and disrupting operations.

During the June–July 2025 heatwave, temperatures exceeded 40 °C in some regions, pushing electricity demand up by 14%. As a result, day-ahead power prices doubled or tripled across major EU markets. According to ECB research, a single summer heatwave can already reduce regional economic output by 1%, with deeper long-term effects over time.

On the opposite extreme, hotter, drier summers are shrinking the Rhine. In July, water levels at the Kaub gauge dropped to a five-year low, forcing barge operators to apply low-water surcharges. Companies like BASF and ThyssenKrupp warned of supply chain delays and cost increases as a result.

Water Excess Is Just as Damaging

In January 2025, thirteen rivers in Wallonia were placed on flood alert, shutting down towpaths and disrupting regional transport. Across the continent, severe flooding made 2024 Europe’s second-costliest flood year on record, with insured losses near €10 billion.

Windstorm Ciarán added to the toll. Occurring from 1–2 November 2023, it caused €2 billion in damages, with Belgium among the hardest-hit. These climate shocks lead directly to business interruption claims, rising insurance premiums, and asset downtime for Belgian companies with operations or suppliers across Western Europe.

Chronic Threats Are Building

Long-term climate pressures, like sea-level rise and water scarcity, are compounding the risks. The Port of Antwerp-Bruges is already planning to raise quay walls by up to three metres and install pump-back systems to handle both storm-surge flooding and Scheldt river droughts. The port reports that Belgium now ranks 18th globally for baseline water stress.

The European Environment Agency’s 2024 Climate Risk Assessment confirms that critical risks to infrastructure, energy, and water security are unfolding faster than adaptation efforts.

For companies, this means it’s essential to integrate physical climate risk analysis into strategic planning now, before the next record-breaking season hits. Delaying ESG data reporting only conceals these vulnerabilities from investors and lenders, until they penalize you for the lack of transparency.

The market is moving - with or without the CSRD obligation

Financial institutions are already adjusting to new rules. The EU “banking package” - CRR III and CRD VI - hard-wires ESG risk into capital requirements, board duties, and supervisory reviews. Banks now need borrower-level data on emissions, building efficiency, and transition plans to run climate-adjusted stress tests and price loans under the EBA’s Loan-Origination Guidelines.

Insurers face parallel pressure as the updated Solvency II framework embeds sustainability risk into underwriting and solvency calculations; weak modelling can even trigger capital surcharges. In short, reliable ESG data is no longer a disclosure nicety, it’s a regulatory necessity.

“We know that ESG data, especially around Scope 3 emissions, is becoming essential, not just for regulatory compliance, but because our clients’ customers and our own reporting obligations are evolving. Even if it’s not yet crystal clear which indicators will be required, when that moment comes, companies will need to respond quickly. That’s why we’re telling clients: start preparing now.” — Johan Thiers, KBC

“We need that data from our clients … otherwise we can’t assess either their carbon footprint or the emissions we finance.” — Hans Stegeman, Triodos Bank

“Investors, pension funds, even banks need the information to understand the risks out there and adjust their portfolios accordingly. The ECB sees climate-heavy loan books as a systemic risk - these disclosures are how we avoid a crisis down the road.” — Richard Gardiner, ShareAction

“If we lessen the data points, the insurance companies wouldn’t have all the data to evaluate climate-change risk when they make the insurance contracts.” — Sirpa Pietikäinen, MEP

“We need data from companies - that’s the point of the CSRD. Less disclosure means we’ll rely even more on costly third-party estimates.” — Ophélie Mortier, DPAM

Even SMEs already reporting see the upside. Bruno Steyaert, CEO at Steyaert-Heene and an early VSME adopter:

“ESG isn’t going away. Some of our biggest clients demand it, and it helps us measure the real impact of what we do.”

From credit lines to supply-chain bids, actionable ESG reporting solutions win business today. Waiting for legal clarity simply hands that edge to faster competitors.

What EU-based SMEs can do now: A future-proof checklist

The rules may still be shifting, but the direction is clear: ESG reporting, especially under the now-endorsed VSME standard, is becoming a baseline expectation, not a nice-to-have. Getting started now doesn’t mean overcommitting. It means future-proofing your business before the pressure hits from all sides.

Will you wait until your bank asks for ESG data during a loan application? Or until your sales team can’t close a deal because buyers demand transparency you can’t provide? Don’t get caught off guard. You don’t want your CEO and CFO blindsided, or your sales team stuck without answers.

If you’re wondering where to begin, here’s a practical path forward:

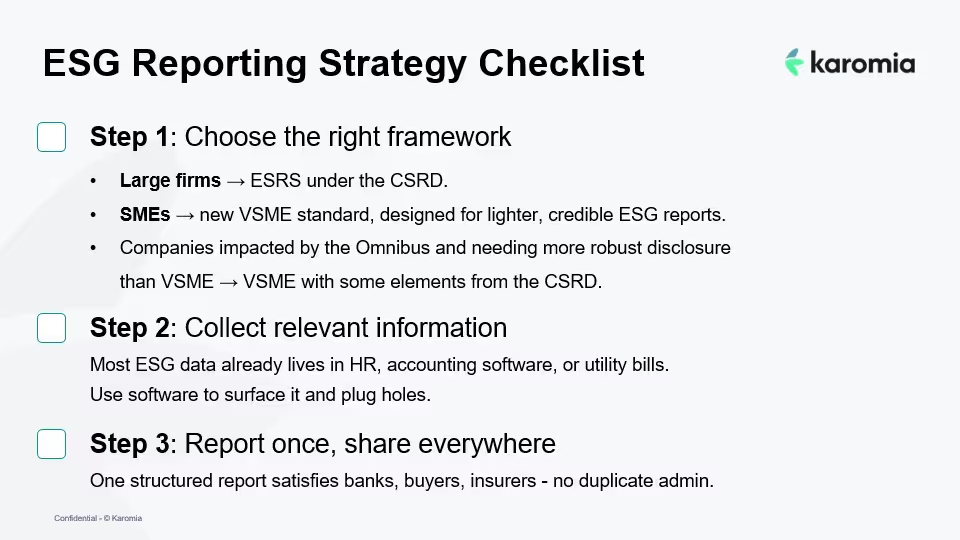

Choose the right path

Start with the framework that fits your size and complexity.

- Large companies should use the ESRS under the CSRD.

- Small and medium-sized enterprises (SMEs) can follow the VSME standard, designed for simpler, credible ESG reports.

- Companies impacted by the Omnibus proposal but needing more robust disclosure than VSME allows can start with VSME and selectively integrate some elements from the CSRD framework.

Collect relevant information

Most companies already have more ESG-relevant data than they think, it’s just stuck in spreadsheets, contracts, or consultant reports. As Bruno Steyaert, CEO at Steyaert-Heene and an early VSME adopter, puts it:

“I could’ve trained for weeks to understand what to report, but it was still just a pile of paper. I could ship those papers to Karomia and they turned them into a fantastic future for us. We could answer all data requests in any format. Now our job is just deciding which documents to upload.”

Learn how Steyaert-Heene uses Karomia to meet ESG data demands.

Report once, and make it count

The European Commission positions VSME as the maximum ESG disclosure reasonably asked of SMEs and now explicitly urges banks and buyers to rely on its KPIs. One VSME report should satisfy your lender, insurer, and clients.

The sooner you start, the smoother it becomes. Begin preparing your ESG report now, and stay one step ahead before your next loan application stalls or a deal gets blocked due to missing ESG data.

👉 Explore Karomia’s ESG Reporting Guide to take the first step.

👉 Ready to future-proof your ESG efforts? Talk to us.

Receive updates and best practices on all things ESG reporting each month.

Read More

.avif)