VSME standard for SMEs: a practical guide to ESG reporting

TL;DR

The VSME (Voluntary Sustainability Reporting Standard for non-listed SMEs) was approved by EFRAG in November 2024 and formally endorsed by the European Commission on 30 July 2025 (Commission Recommendation 2025/1710). It is a free, modular ESG reporting standard built specifically for non-listed micro, small, and medium-sized enterprises. It is not legally mandatory, but it is rapidly becoming the common language that banks, large corporates, and investors use when they ask you for ESG data.

Following the Omnibus I Directive (24 February 2026), a new value chain cap means large companies subject to CSRD can no longer demand more ESG data from their suppliers than what the VSME specifies. That's legal protection you can use today.

What is the VSME standard?

The VSME is a voluntary sustainability reporting standard developed by EFRAG (the European Financial Reporting Advisory Group) for non-listed micro, small, and medium-sized enterprises. EFRAG approved the final VSME standard on 13 November 2024, and the European Commission formally endorsed it on 30 July 2025 via Commission Recommendation 2025/1710.

It was developed as part of the European Commission's SME Relief Package (September 2023) — a direct response to the growing wave of ESG questionnaires that SMEs were drowning in. The goal was simple: give SMEs one standard they can use to answer all those requests, rather than filling out a different form for every bank, buyer, and investor they work with.

Why the VSME exists in practice

Large companies reporting under CSRD need sustainability data from their value chains. Belgian companies set some of Europe's most ambitious climate targets. But most of the emissions? They sit upstream with SMEs.

Banks need ESG data from their SME clients to manage their own regulatory obligations (Pillar 2, Pillar 3, SFDR). These organisations aren't asking SMEs for ESG data to create admin. They're helping them stay competitive and financeable in a world where this data will soon be table stakes. Omnibus changed timing, not direction.

Until now, large companies are missing supplier data and banks use proxy data. The VSME replaces most of that. The public consultation confirmed that VSME reporting can cover up to 80% of what business partners typically request.

Who is the VSME for?

The VSME standard applies to non-listed undertakings. It covers three size categories:

- Micro-undertakings: below €450,000 balance sheet / €900,000 turnover / 10 employees (meeting any 2 of 3)

- Small undertakings: below €5M balance sheet / €10M turnover / 50 employees (meeting any 2 of 3)

- Medium-sized undertakings: below €25M balance sheet / €50M turnover / 250 employees (meeting any 2 of 3)

Note: these balance sheet and turnover thresholds reflect the updated figures from the EC's Delegated Act amending Directive 2013/34/EU, applicable from January 2024 (reporting year 2025).

Why does VSME reporting matter now?

The value chain cap is real

The Omnibus I Directive (adopted 24 February 2026) introduced a legal value chain cap: large companies subject to CSRD cannot require their SME suppliers to provide sustainability data beyond what the VSME standard specifies. Contracts that try to impose stricter requirements are legally void. If you are an SME, you now have formal protection against being buried in excessive ESG data requests from large clients.

Banks are already requesting VSME data

Financial institutions need ESG data to fulfil their own obligations — from the EBA's Pillar 2 and Pillar 3 requirements to SFDR principal adverse impact (PAI) indicators. The VSME was designed with the banking sector's data needs explicitly in mind. The Comprehensive Module covers the full set of SFDR PAI Table 1 indicators, the Benchmark Regulation datapoints, and the EBA Pillar 3 datapoints — which means a completed VSME report directly satisfies what your bank is likely asking for.

In Belgium, Kube, developed by Isabel and Karomia, is already used by Belgium's four major banks and public investors. With support from leading corporates, it's ready to scale and bring credible ESG and emissions data to the Belgian SME ecosystem, making it easier for both sides to work with the same data in the same format.

Your supply chain position depends on VSME compliance

Large corporates subject to CSRD need Scope 3 emissions data from their suppliers. Without credible data from you, they either use rough proxies (which often penalise suppliers unfairly) or ask for it through their own questionnaires. A VSME sustainability report gives them what they need in a format they can actually use.

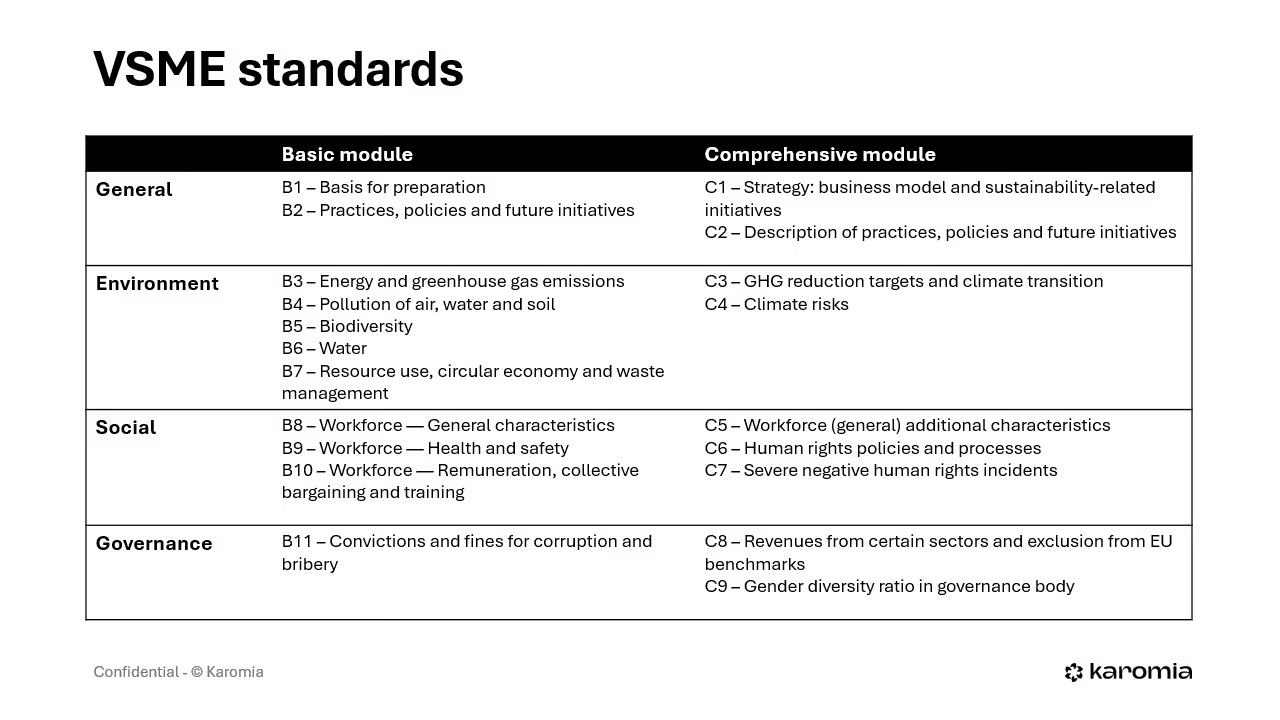

The two VSME modules explained

The VSME has a modular structure. You can use the Basic Module alone, or combine it with the Comprehensive Module depending on the ESG data demands you face.

VSME Basic Module

The entry level for SME sustainability reporting. Designed as the target for micro-undertakings, and the minimum requirement for all other SMEs. Uses simplified language. No materiality analysis required. Instead, an "if applicable" principle filters which disclosures are relevant to your specific situation.

All disclosures must be reported on if applicable. The Basic Module covers:

General information

- B1 – Basis for preparation: legal form, NACE sector code(s), balance sheet total, turnover, employee count (FTE or headcount), primary country of operations, geolocation of sites, ESG certificates

- B2 – Practices, policies and future initiatives: whether the undertaking has sustainability practices, policies, or future initiatives in place, and whether these are supported by targets

Environmental metrics

- B3 – Energy and greenhouse gas emissions: total energy consumption (breakdown by renewable/non-renewable), Scope 1 and location-based Scope 2 GHG emissions in tCO₂eq, GHG intensity (emissions per euro of turnover)

- B4 – Pollution of air, water and soil: pollutants emitted to air, water and soil (if already required by law or voluntarily reported under an Environmental Management System)

- B5 – Biodiversity: number and area (in hectares) of sites in or near biodiversity-sensitive areas

- B6 – Water: total water withdrawal and (where applicable) water consumption

- B7 – Resource use, circular economy and waste management: application of circular economy principles, annual waste generation (hazardous/non-hazardous breakdown), waste diverted to recycling or reuse, annual mass flow of significant materials (for manufacturing, construction and/or packaging)

Social metrics

- B8 – Workforce — General characteristics: total employees by contract type, gender, and country; employee turnover rate (threshold: 50 employees)

- B9 – Workforce — Health and safety: number and rate of recordable work-related accidents; fatalities from work-related injuries and ill health

- B10 – Workforce — Remuneration, collective bargaining and training: whether employees receive at least the applicable minimum wage; gender pay gap (threshold: 150 employees, reducing to 100 from 7 June 2031); percentage covered by collective bargaining agreements; average annual training hours per employee by gender

Governance metrics

- B11 – Convictions and fines for corruption and bribery: number of convictions and amount of fines for anti-corruption and anti-bribery violations (if any)

VSME Comprehensive Module

For SMEs facing more detailed ESG data requests from banks, investors, and large corporates. Built on top of the Basic Module — you need to complete Basic first.

The Comprehensive Module covers the full SFDR PAI Table 1 indicators, EBA Pillar 3 datapoints, and the Benchmark Regulation requirements. Uses the same "if applicable" principle as the Basic Module (the materiality analysis that existed in the original Exposure Draft was removed following the public consultation).

General information

- C1 – Strategy: business model and sustainability-related initiatives: description of products/services, markets, and business relationships; key sustainability-related initiatives

- C2 – Description of practices, policies and future initiatives: narrative descriptions of the sustainability practices and policies declared in B2; governance responsibilities; whether targets exist and who at senior level is accountable

Environmental metrics

- Scope 3 GHG emissions consideration: for undertakings in high-emission sectors, an entity-specific disclosure on Scope 3 emissions (not mandatory, but encouraged where relevant)

- C3 – GHG reduction targets and climate transition plan: emission reduction targets for Scope 1 and 2 (and Scope 3 if set); for high climate impact sectors, a voluntary transition plan for climate change mitigation

- C4 – Climate risks: description of climate-related hazards and transition events; exposure and sensitivity of assets, activities and value chain; time horizons; climate change adaptation actions taken

Social metrics

- C5 – Workforce (General) additional characteristics: female-to-male ratio at management level (voluntary; threshold: 50 employees); number of self-employed and temporary agency workers (voluntary)

- C6 – Human rights policies and processes: whether a code of conduct or human rights policy exists for own workforce; complaints-handling mechanism

- C7 – Severe negative human rights incidents: confirmed incidents of child labour, forced labour, human trafficking, or discrimination in own workforce; awareness of incidents in value chain, affected communities, or consumers

Governance metrics

- C8 – Revenues from certain sectors and exclusion from EU benchmarks: revenues from controversial weapons, tobacco, fossil fuels, or agrochemicals; whether excluded from EU Paris-aligned reference benchmarks

- C9 – Gender diversity ratio in governance body: ratio of female to male members of the governance body (if one exists)

Key principles for VSME preparation

The "if applicable" principle

The materiality analysis was removed from the VSME following extensive feedback from both preparers and users. Instead, the standard uses an "if applicable" approach: if your circumstances are different from those that would trigger a specific disclosure, you simply don't report on it. The guidance explains clearly when each VSME disclosure becomes applicable.

No cherry-picking

Once you choose a VSME module, you report on all applicable disclosures within it. You can add selected disclosures from the other module, or include entity-specific and sector-specific information, but you can't skip disclosures that are applicable to you.

Consolidated reporting

Where relevant, the VSME report should include subsidiaries. If your parent company already includes your data in its consolidated sustainability report, you may be exempt from separate VSME reporting.

Annual reporting

VSME reports should be prepared annually, if your business partners request this. If data has not changed from the previous year, you may refer to the previous period and state this explicitly.

Comparative information

From the second year of VSME reporting, you should include comparative data from the prior year. This is a standard principle that applies across both modules.

Sensitive information

If disclosing certain information would require revealing classified or sensitive data, you may omit it. You simply state that this is the case in B1.

Where to publish your VSME report

You can include the VSME report as a section of your management report, attach it to your financial statements, or publish it as a separate document. Nothing prevents you from making it publicly available, but the primary purpose is to share it with specific business counterparts.

How to do your VSME with Kube

You have two options when it comes to completing your VSME report. You can work through it manually — collecting data, filling in templates, and sharing documents by email. Or you can use Kube.

Kube is the Belgian national ESG data exchange platform, created on the initiative of Febelfin and Isabel in partnership with Karomia, with advice from federations, public investment institutions (Wallonie Entreprendre, PMV, LRM, SFPIM), and banking partners (ING, BNP Paribas Fortis, Belfius, KBC, and others). It was launched in November 2025. In 2026, use of Kube is free for SMEs.

The four steps to complete your VSME report with Kube

Step 1 – Sign up on the platform

Register securely using your company number or itsme®.

Step 2 – Import your ESG data with the help of AI

Annual reports, energy bills, employee policies — with one click, AI can automatically fill in up to 80% of your VSME report based on your existing documents.

Step 3 – Review, adjust, and complete the remaining fields

As long as the report is not finalised, you can fully edit and update it.

Step 4 – Get your VSME report

After validation, you receive a PDF sustainability report that meets the European VSME framework, ready to share with banks, customers, or partners. All while you keep full control over your data. One VSME report, recognised everywhere.

Frequently asked questions

Is VSME reporting legally binding?

The VSME itself is voluntary. However, Commission Recommendation 2025/1710 gives it formal standing, and the Omnibus I Directive requires the Commission to adopt it as a formal delegated act within 4 months of the Directive entering into force. That delegated act will give it full legal standing. More importantly: even though VSME reporting is voluntary, the value chain cap that protects SMEs from excessive ESG data requests is legally binding now.

Can my bank require me to complete a VSME report?

Your bank can request sustainability information from you. If the VSME is adopted as a delegated act, banks and large companies cannot demand more than what the VSME covers. That said, many banks are actively encouraging VSME adoption through Kube because it reduces their own ESG data collection burden.

Do I need to do a materiality analysis for the VSME?

No. The materiality analysis was removed from the VSME following the public consultation. The "if applicable" principle replaces it — simpler, clearer, and proportionate for SMEs.

What happens if my company grows beyond the SME thresholds?

If you exceed the medium-sized undertaking thresholds (balance sheet above €25M, turnover above €50M, employees above 250) for two consecutive financial years, you become a large undertaking and may fall under mandatory CSRD reporting requirements. The same applies in reverse: a large undertaking that falls within SME thresholds for two consecutive years becomes an SME and can apply the VSME.

How long does VSME reporting take?

Based on field test evidence, most SMEs can complete the VSME Basic Module in a few hours once they have their data organised. The Comprehensive Module takes longer, particularly for disclosures like C3 (GHG reduction targets and climate transition plan) and C4 (climate risks). Using Kube significantly reduces the time required, particularly from the second year of reporting.

Does the VSME replace EMAS or GRI reporting?

No. The VSME and EMAS serve different purposes. References to EMAS were removed from the main text of the VSME standard following the public consultation, as EMAS was considered too complex for most SMEs and too narrow in focus. Nothing prevents you from holding an EMAS certification alongside your VSME report. For GRI reporters: the VSME covers similar ground on many sustainability topics but uses EU-specific definitions and SFDR-aligned datapoints that GRI does not.

Can I include sector-specific information in my VSME report?

Yes, and in some cases you should. The VSME is sector-agnostic by design, but you can add entity-specific or sector-specific disclosures where relevant to your business. EFRAG has indicated it may develop sector guidance in future as part of its ongoing sector programme.

The VSME was approved by the EFRAG Sustainability Reporting Board on 13 November 2024 and endorsed by the European Commission on 30 July 2025 via Commission Recommendation 2025/1710.