Simplified ESRS: what changed, what still matters, and what to do next

TL;DR

“Simplified ESRS” is an easy label to misread. There are fewer datapoints, a clearer structure, and more realistic timelines under CSRD — but the bar didn’t move. Companies making progress are using the extra time to tighten their double materiality assessment, run early draft reports, and build audit-ready processes step by step. If you wait for things to feel “final”, you’ll run out of runway.

Over the past year, many sustainability teams slowed down.

Not because they didn’t care, but because the rules kept moving. During the Omnibus discussions in 2025 and ongoing clarifications from EFRAG, many companies chose to pause rather than build something they might have to undo.

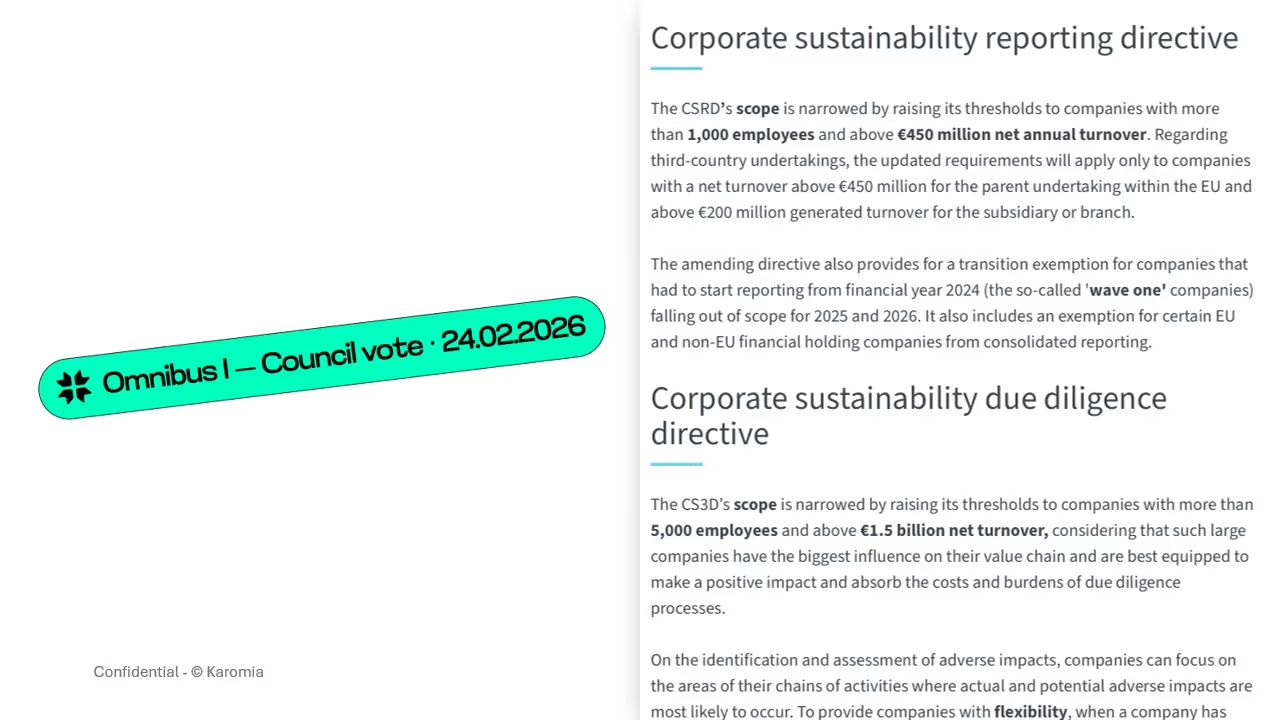

That changed on 3 December 2025, when EFRAG published the draft amended ESRS — what most people now call “simplified ESRS”.

In our conversations with customers, the question shifted almost overnight:

From: “What if this changes again?”

To: “What can we realistically do now?”

This article reflects what we’re seeing companies do in practice today.

What “simplified ESRS” actually means

Simplified ESRS is about clarity and usability — not reduced ambition.

In practical terms, it means:

- Fewer datapoints

- Less repetition

- A consistent structure linking material topics to policies, actions, and targets

The goal isn’t lighter work. It’s sharper insight.

How many datapoints were removed?

This is where the change is most visible: datapoints dropped by roughly 70%, from about 1,200 to just over 300.

For most teams, this has an immediate effect: less time chasing marginal datapoints, more time improving the quality of what actually matters.

Does simplified ESRS lower expectations?

No. And this is where some teams still get it wrong. Simplified does not mean easier.

There’s more noise than ever — but the bar hasn’t moved. Auditors and regulators still expect:

- Clear logic

- Traceable decisions

- Strong links between risks, policies, actions, and targets

With fewer datapoints, each one simply matters more.

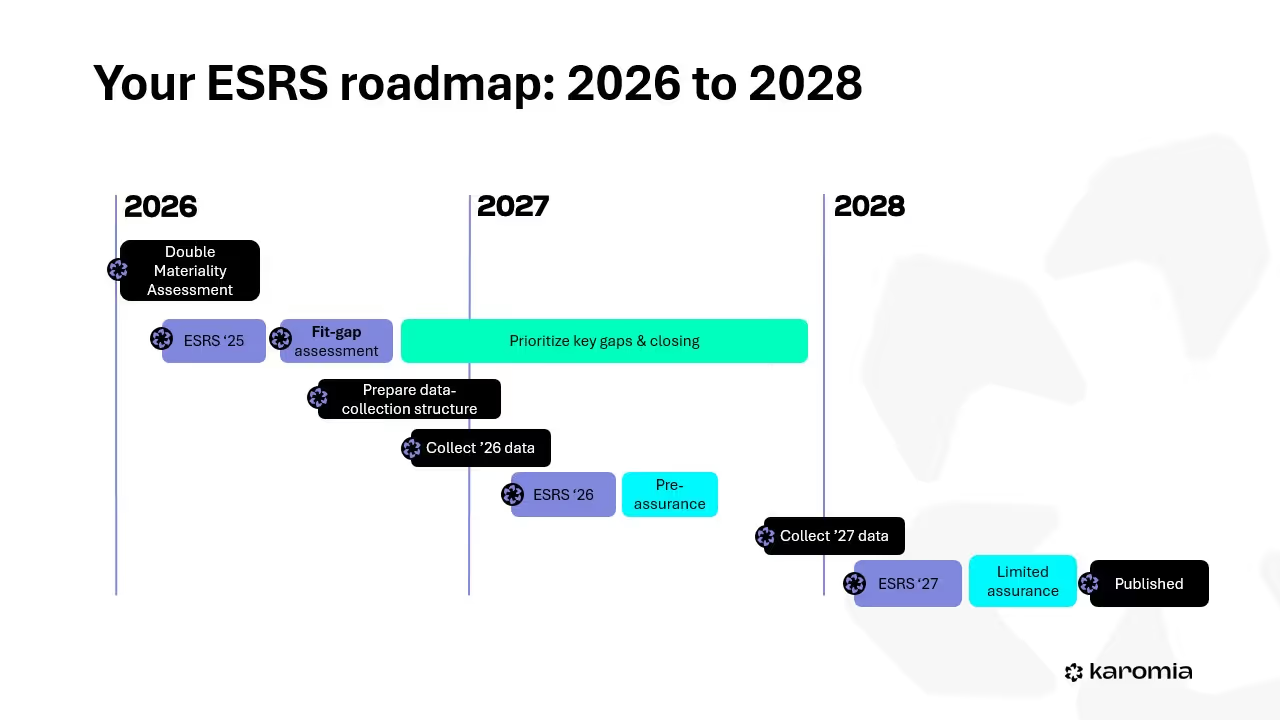

The timeline companies are working with

Most organisations are now effectively on a stop-the-clock trajectory under CSRD, with first ESRS reporting expected in 2028, based on 2027 data.

That creates a three-year runway. How you use it makes all the difference.

How we suggest using the time

2026: build the foundation

Treat 2026 as a reality check.

What we see working:

- Run or refresh your double materiality assessment

- Produce a first draft ESRS report

- Identify missing policies, data gaps, and documentation needs

The draft doesn’t need to be perfect. Its job is to show you where things break.

2027: dry run and refine

In 2027, you repeat the exercise — with better data and clearer narratives.

This is when:

- Datasets improve

- Storylines mature

- Processes start aligning with assurance expectations

By the end of this phase, reporting feels manageable. Not rushed.

2028: assurance

If you’ve done the work earlier, 2028 isn’t dramatic.

You enter assurance with tested processes, clear documentation, and far less pressure on internal teams.

Why double materiality still sits at the centre

Even with simplification, double materiality remains the foundation.

It decides:

- What you report on

- What you don’t

- Where effort and resources go

What has changed is how teams approach it.

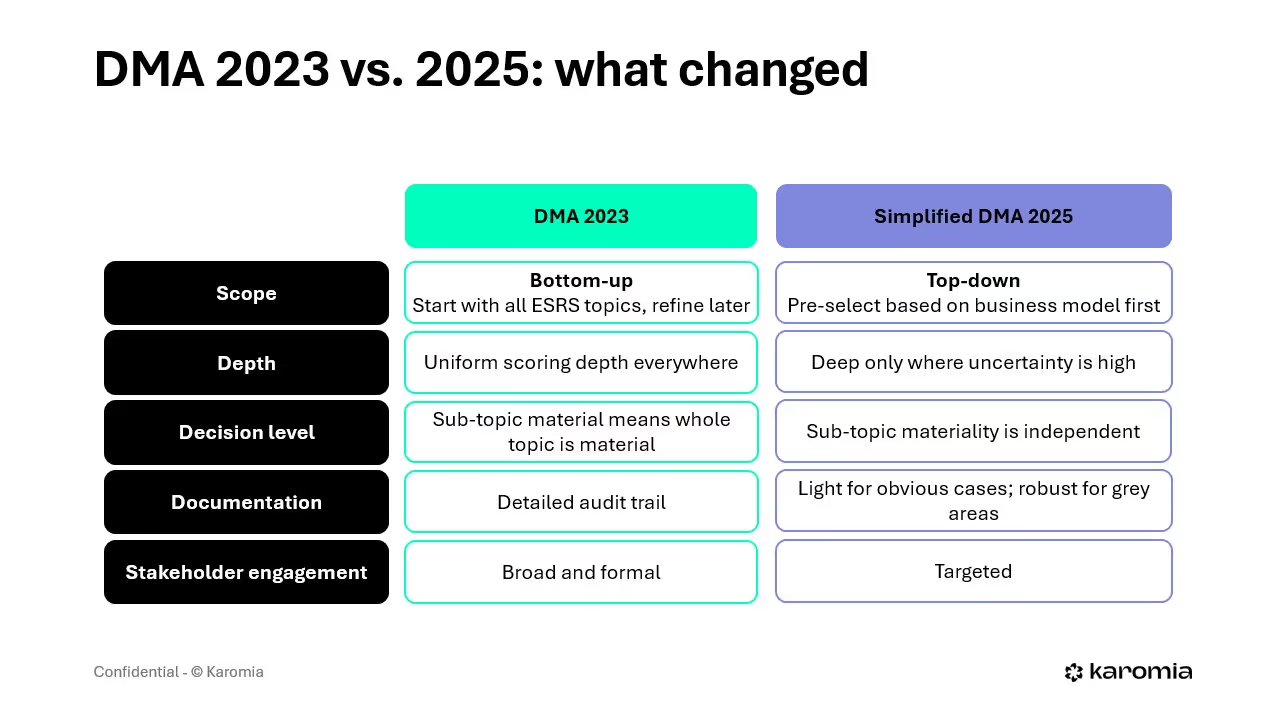

What changed in the DMA approach

Early ESRS projects followed a pattern that didn’t scale well: bottom-up, too detailed, too heavy.

Teams assessed:

- Too many topics

- Too many impacts, risks, and opportunities

- Too much low-value information

Simplified ESRS pushes a more top-down logic:

- Start from the business model and value chain

- Narrow down to what is genuinely relevant

- Focus effort where materiality is uncertain

Less volume. Better judgement.

What we see in practice

Across multiple DMA projects, three patterns show up consistently.

1. Less scope, same result

At one mid-sized manufacturing company:

- Topics assessed dropped from 10 to 7

- The final outcome stayed the same: 5 material topics

The difference wasn’t the result. It was the effort needed to get there.

2. Fewer IROs, better insight

- Old approach: 600+ IROs reviewed

- Simplified approach: fewer than 300

Teams stopped analysing items that added complexity without improving decisions.

3. More focused stakeholder input

- Old approach: 2,000+ survey responses

- Simplified approach: ~500 targeted inputs

Expert interviews and workshops produced clearer insight exactly where uncertainty existed.

Documentation still matters

One thing we repeat often: simpler does not mean undocumented.

Materiality decisions — especially exclusions and grey areas — still need to be clearly recorded. This creates:

- A solid audit trail

- Internal alignment

- Less friction during assurance

A clearer report structure

Simplified ESRS also fixes a structural problem.

Every material topic now follows the same logic:

Policies → Actions → Targets

The result:

- Less duplication

- Easier navigation

- Reports that are easier to read and easier to audit

Old vs simplified ESRS in practice

We ran the same ESRS report twice for a listed Belgian company, using only public information, once under the old standards and once under simplified ESRS.

The difference was immediate.

Under the old ESRS, the draft contained 411 datapoints and ran over 48,000 words.

Under simplified ESRS, that dropped to 194 datapoints — a 53% reduction — and fewer than 19,000 words.

At the same time, the share of clearly structured datapoints increased from 40% to 67%.

Why early draft reporting works

We generated a draft ESRS report in under an hour using public information only.

The result:

- 65% of datapoints incomplete

- Immediate visibility on missing policies, data, and documentation

That’s not a failure. It’s a diagnostic.

Early drafts show you where to focus, before pressure builds.

The mistake we still see

Some organisations treat simplification as a reason to wait.

It’s the opposite.

Simplified ESRS gives you the chance to spread effort over time, improve quality, and avoid last-minute stress. The teams that start now are the ones who will feel comfortable in 2028.

From what we see:

- Simplified ESRS creates breathing room, not shortcuts

- A strong DMA still does the heavy lifting

- Early draft reporting creates clarity

- Technology helps remove unnecessary bureaucracy

Done well, simplified ESRS becomes structured, traceable, and genuinely useful — not just compliant.

Receive updates and best practices on all things ESG reporting each month.

Read More

.avif)